6. E-Checking.

What is an E-Check?

An E-Check (or electronic check) is an electronic version of a paper check used to make payments online. Anyone with a checking account can pay by E-Check through CitePayUSA.

To make a payment with an E-Check, you simply provide the following information:

●Your bank routing number*

●Your bank account number*

●The name on your bank account*

●Your bank account number*

●The name on your bank account*

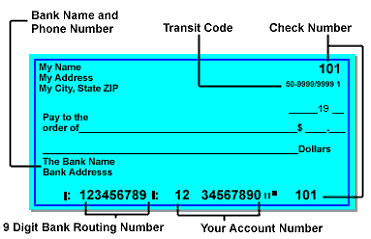

The bank information needed is your -digit routing number and your checking account number.

Well, banks aren't the only businesses using electronic means to process paper checks. Increasingly, consumers are finding that their checks are being electronically converted by retailers, credit card companies and other companies that need to be paid. This process is known as “electronic check conversion.”

Under electronic check conversion, your check is simply used to obtain information – bank routing number, check number, etc. – to process your purchase or payment. All that information is used to make an electronic withdrawal from your account using the Automated Clearing House (ACH) network.

Electronic check conversion is becoming widely adopted by many companies because it speeds up their payment and reduces the cost of processing paper checks.

.

Your check can be converted whether you're standing in the store making a purchase or mailing it to pay a bill. For example, you may buy something and write a check. But instead of the clerk placing your check in her cash register drawer, she scans it and returns the check to you. If this has happened to you, your check was electronically converted. In some cases, you might not have needed to even fill out the check.

When retailers or businesses use check conversion, your payment may be processed a lot faster than if they sent your check through the traditional way. So be sure you have enough money in your account at the time you make your purchase or pay your bill.

Now, don't go worrying yourself that businesses will have carte blanche to raid your checking account. The company billing you will still have to go through your bank or credit union. Also, for your protection, if you mail a check and the company converts it to an e-check, the original check has to be destroyed within 14 days. “This prevents double billing,” said Michael Herd, the spokesman for NACHA. But the company has to keep a copy of the check for two years as required by NACHA rules.

Herd also points out that consumers have better protections for electronic fund transfers, which is what e-checks are, than for checks processed the traditional way. For example, with electronic check conversion you have the right to an investigation by your financial institution when an error occurs.

If a business is using electronic check conversion, it has to tell you upfront, as required by the federal Electronic Fund Transfer Act. You may see a notice at the cash register in the store or you may get something in your monthly credit card statement.

And by the way, if a company is converting mailed checks to e-checks, it has to allow consumers to opt-out. Just call and ask. Herd said only one percent of people do opt out.

Here are some things to pay attention to when it comes to electronic check conversion, according to the Federal Trade Commission and Federal Reserve Board:

Review your checking account statement to be sure a check was processed electronically only once and for the correct amount.

●If you do find unauthorized or incorrect electronic transfers on your account, notify your financial institution immediately. Getting your money back or correcting the error will depend on how quickly you report the problem. You have only 60 days (from the date your statement was sent) to tell the financial institution about the error.

●For checks processed electronically in a store, make sure you keep a copy of the check handed back to you in case you need proof of payment. That check will have been voided in some sort of way. Also, hold on to your receipt, which should include the date of the transaction, the amount, location and name of merchant.

●If you mail a check and a company electronically converts it, you won't get your check back. So keep your checking account statements with information about electronically processed purchases and payments. However, if you need a copy of your check, contact the billing company, which has to give you one

how do e-checks work

Electronic checks are designed to accommodate the many individuals and entities that might prefer to pay on credit or through some mechanism other than cash electronic checks are modeled on paper checks, except that they are initiated electronically, use digital signatures for signing and endorsing, and require the use of digital certificates to authenticate the payer, the payer’s bank and bank account. The payer writes the e-check through a computer, uses a digital signature and sends it either by direct transmission using telephone lines or by public networks such as the Internet. The payee receives it, verifies signatures, endorses it, writes a deposit slip, and signs it. The endorsed check is then sent over internet to the payee's bank for deposit. Bank personnel verify signatures, credit the deposit, and then clear and settle the endorsed e-check by sending it on to the payer's bank, where signatures are once again verified and the amount of the e-check is debited from the payer's account. The cryptographic certificates used with an e-check enable a check payee to determine the validity of the signatures. Initially, these certificates are actually transmitted with the e-check, but alternative models where the transmission, or possibly even issuance, of the certificate is not required are currently in the making. e-check technology also allows digital signatures to be applied to document blocks, rather than to the entire document. This allows parts of a document to be separated from the original, without compromising the integrity of the digital signature.

Benefits of Electronic Checks

●Reduce bad check write-offs, returned-check fees and check collection hassles

●Improved cash flow

●Eliminates bank processing fees

●Reduced deposit preparation time

●Online reporting through secured web-based network

●Reduced accounting requirements

●Flexible solutions to check processing

●Funds available to merchant within two banking days

●Check verification and authorization through nationwide database

●Large national negative database

●ID-based check fraud protection available

●Positive scoring database

●Merchant selected check acceptance controls