2. Using payment cards online.

payment card

Electronic card that contains information that can be used for payment purposes

●Payment cards come in three types:

●Credit cards : provide the holder with credit to make purchases up to a limit fixed by the card issuer

●Charge cards :the balance on a charge card is supposed to be paid in full upon receipt of the monthly statement

● Debit cards : with a debit card , the money for a purchased item comes directly out of the holder’s checking account

●Payment cards come in three types:

●Credit cards : provide the holder with credit to make purchases up to a limit fixed by the card issuer

●Charge cards :the balance on a charge card is supposed to be paid in full upon receipt of the monthly statement

● Debit cards : with a debit card , the money for a purchased item comes directly out of the holder’s checking account

Charge Card vs. Credit Card Cost

You won’t pay any interest on a charge card balance because you’re not allowed to carry a balance beyond the grace period. However, you’ll face a late fee if your full balance isn’t paid by the due date, the late fee could be a flat fee or a percentage of your balance. Credit cards also have a late fee that’s charged when you don’t make your minimum payment by the due date.

Processing Cards Online

authorization

Determines whether a buyer’s card is active and whether the customer has sufficient funds

settlement

Transferring money from the buyer’s to the merchant’s account

Three basic configurations for processing online payments.

Merchants may:

Own the payment software :

A merchant can purchase a payment-processing module and integrate it with its other EC software

●In online marketing, a shopping cart is a piece of e-commerce software on a web server that allows visitors to an internet site to select items for eventual purchase

●The software allows online shopping customers to accumulate a list of items for purchase, described metaphorically as “placing items in the shopping cart” or “adding to cart”. Upon checkout, the software typically calculates a total for the order, including shipping and handling (i.e. postage and packing) charges and the associated taxes, as applicable.

●In online marketing, a shopping cart is a piece of e-commerce software on a web server that allows visitors to an internet site to select items for eventual purchase

●The software allows online shopping customers to accumulate a list of items for purchase, described metaphorically as “placing items in the shopping cart” or “adding to cart”. Upon checkout, the software typically calculates a total for the order, including shipping and handling (i.e. postage and packing) charges and the associated taxes, as applicable.

Use a point of sale system (POS) operated by an acquirer :

Merchants can redirect cardholders to a POS run by an acquirer

In recent years, a number of companies have offered Apple-centric POS systems for hospitality and retail including Revel Systems, Prosperity POS, Lavu POS, ShopKeep POS, LightSpeed, and SalesVu. Some of these function similar to traditional POS systems using client-server models, while newer systems can run in the cloud on iOS based devices.

The advantages of a cloud-based POS are instant centralization of data, ability to access data from anywhere there is internet connection, and lower costs.[7][8] Cloud-based POS also helped expand POS systems to mobile devices.

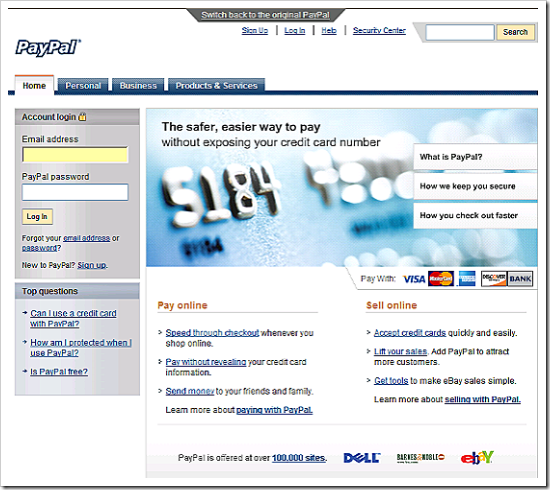

+ PayPal is the world’s most widely used payment acquirer, PayPal payments are made using a user’s existing account or with a credit card. Money can be sent directly to an email address, thus prompting the users to sign up for a new PayPal account. In addition to taking payments, PayPal also allows its users to send money through the service, which is a feature that only a few payment solutions provide.

In recent years, a number of companies have offered Apple-centric POS systems for hospitality and retail including Revel Systems, Prosperity POS, Lavu POS, ShopKeep POS, LightSpeed, and SalesVu. Some of these function similar to traditional POS systems using client-server models, while newer systems can run in the cloud on iOS based devices.

The advantages of a cloud-based POS are instant centralization of data, ability to access data from anywhere there is internet connection, and lower costs.[7][8] Cloud-based POS also helped expand POS systems to mobile devices.

+ PayPal is the world’s most widely used payment acquirer, PayPal payments are made using a user’s existing account or with a credit card. Money can be sent directly to an email address, thus prompting the users to sign up for a new PayPal account. In addition to taking payments, PayPal also allows its users to send money through the service, which is a feature that only a few payment solutions provide.

Use a POS operated by a payment service provider (PSP) :

PSP is a third-party service connecting a merchant’s EC system to the appropriate acquiring bank or financial institution. PSPs must be registered with the various card associations they support.

● Since 1996, managing the submission of billions of transactions to the processing networks on behalf of merchant customers

●merchants can easily connect to the Authorize.Net Payment Gateway, which provides the complex infrastructure and security necessary to ensure fast, reliable and secure transmission of transaction data. Authorize.Net manages the routing of transactions just like a traditional credit card swipe machine you find in the physical retail world, however, Authorize.Net uses the Internet instead of a phone line.

● Since 1996, managing the submission of billions of transactions to the processing networks on behalf of merchant customers

●merchants can easily connect to the Authorize.Net Payment Gateway, which provides the complex infrastructure and security necessary to ensure fast, reliable and secure transmission of transaction data. Authorize.Net manages the routing of transactions just like a traditional credit card swipe machine you find in the physical retail world, however, Authorize.Net uses the Internet instead of a phone line.

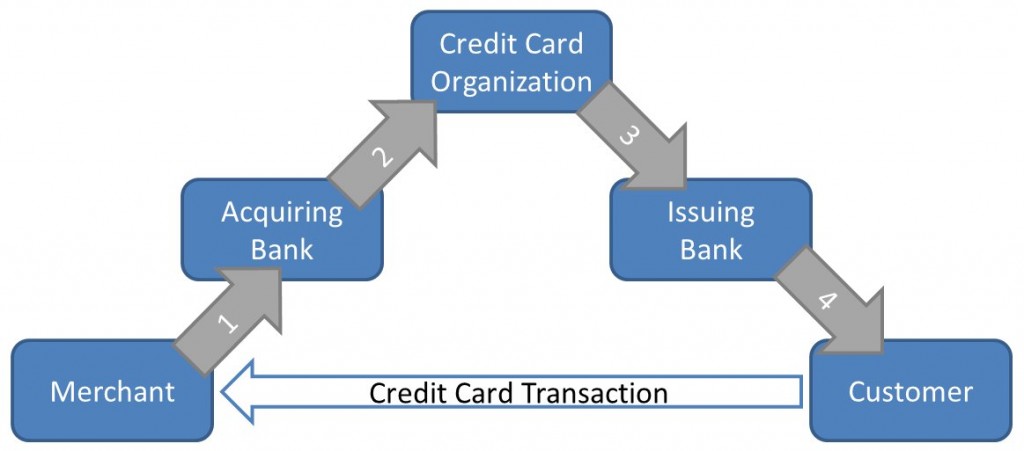

The key participants in processing card payments online include:

Acquiring bank : offers special account called an internet merchant account that enables card authorization and payment processing .

Credit card association : the financial institution providing card services to banks (e.g. Visa , MasterCard)

Customer : the individual possessing the card.

Issuing bank : the financial institution that provides the customer with the card

Merchant : a company that sells products or services.

Payment processing service : a service that provides a connectivity among merchants , customers , and financial networks , which enables authorization and payments.

Processor : the data center that processes card transactions and settles funds to merchants .

Credit card association : the financial institution providing card services to banks (e.g. Visa , MasterCard)

Customer : the individual possessing the card.

Issuing bank : the financial institution that provides the customer with the card

Merchant : a company that sells products or services.

Payment processing service : a service that provides a connectivity among merchants , customers , and financial networks , which enables authorization and payments.

Processor : the data center that processes card transactions and settles funds to merchants .

Authorize.Net has been a leading provider of payment gateway services

Fraudulent Card Transactions

●In the online world, merchants are held liable for fraudulent transactions

●Merchants can incur additional fees and penalties imposed by the card associations

●Costs associated with combating fraudulent transactions are also the merchant’s responsibility

●Merchants can incur additional fees and penalties imposed by the card associations

●Costs associated with combating fraudulent transactions are also the merchant’s responsibility

The key tools used in combating fraud:

●Address Verification System (AVS)

Detects fraud by comparing the address entered on a Web page with the address information on file with the cardholder’s issuing bank(is a system used to verify the address of a person claiming to own a credit card. The system will check the billing address of the credit card provided by the user with the address on file at the credit card company)

●Manual review

These analysts review orders and get in touch with customers and payment providers to verify that orders are not fraudulent. This technique should be used in conjunction with risk prediction models and rules based detection. This ensures that the fraud analysts only look at focused subset of orders having a high likelihood of being fraudulent . while manual review may be viable for smaller merchants with low order volume because it's expensive.

Asking some of the questions below can help identifying the possible fraudulent orders:

1. Are the goods of high value or easily resalable?

2. Is the sale too easy for a new customer?

3. Is the sale excessively high in comparison with your usual orders?

4. Is the customer ordering many different items?

5. Is the customer reluctant to provide a fixed line number?

6. Does the address provided seem suspicious?

7. Has the delivery address been used before with different customer details?

8. Is it a repeat order shortly after the initial one?

9. Is it an international order that originated from High Risk Country?

10. Is ship-to address same as the billing address?

2. Is the sale too easy for a new customer?

3. Is the sale excessively high in comparison with your usual orders?

4. Is the customer ordering many different items?

5. Is the customer reluctant to provide a fixed line number?

6. Does the address provided seem suspicious?

7. Has the delivery address been used before with different customer details?

8. Is it a repeat order shortly after the initial one?

9. Is it an international order that originated from High Risk Country?

10. Is ship-to address same as the billing address?

●Fraud screens and automated decision models

These system apply a merchant’s business rules to evaluate risk on incoming orders in real-time. This system can help organizations quickly analyze data from incoming transactions and assess their risk , thereby enabling merchants to scale their business as order volumes increase. And because fraud patterns are dynamic , automated screening systems allow merchants to implement changes quickly.

●card verification number (CVN)

Detects fraud by comparing the verification number printed on the signature strip on the back of the card with the information on file with the cardholder’s issuing bank

Address verification is both an automated and procedural fraud prevention technique that all online merchants can use to reduce credit card fraud and theft, this process requires that the card be physically present at the time of the transaction thus reducing card not present fraud scenarios.

An example is the eBay auction process. When checking out and preparing to pay for the auction, shipping and billing addresses are made available to the seller. Matching this information can lead to a better level of fraud prevention and can save the seller significant money, time, and effort. The automated systems work in the same manner and perform the check online and in the background and are extremely accurate.

An example is the eBay auction process. When checking out and preparing to pay for the auction, shipping and billing addresses are made available to the seller. Matching this information can lead to a better level of fraud prevention and can save the seller significant money, time, and effort. The automated systems work in the same manner and perform the check online and in the background and are extremely accurate.

●Card association payer authentication services

Payer Authentication (also known as 3-D Secure) is a solution created by the credit card associations to provide additional fraud protection by asking cardholders to authenticate themselves to their issuing bank at the time of purchase. A cardholder’s identity is confirmed using one of a variety of authentication methods, and merchants are provided with instant authentication results thereby greatly reducing the risk of unauthorized use.

Advantages:

Reduces Fraud – Merchants can verify that the person using the card is the cardholder.

Charge-back Protection – Authenticated transactions may not be charged back if the cardholder alleges they did not make or authorize the purchase.

Increases consumer confidence – Assures consumers that their transactions will be secure, leading to increased sales.

Reduces Fraud – Merchants can verify that the person using the card is the cardholder.

Charge-back Protection – Authenticated transactions may not be charged back if the cardholder alleges they did not make or authorize the purchase.

Increases consumer confidence – Assures consumers that their transactions will be secure, leading to increased sales.

How does the payer authentication process work?

Consumers enroll their Visa or MasterCard credit cards in the Verified by Visa or MasterCard SecureCode programs at their issuing bank's web site. During the enrollment, they choose a password to associate with their card. When they use that card at a merchant enabled for Verified by Visa and MasterCard SecureCode, they are prompted by their issuing bank to 'sign" for the purchase with their password.

●Negative lists

These lists typically define the set of minimum criteria an order transaction must satisfy before proceeding for fulfillment . these consists of lists known fraudulent data such email ids , stolen credit card numbers , bad shipping address etc. these files are based on past experiences , data mining of fraudulent orders and periodic updates by credit card companies .